The 2026 financial year presents several valuable tax planning opportunities for small and medium-sized businesses. Many of these concessions are changing or becoming less generous from 1 July 2026, making proactive planning particularly important.

2026 Year-End Tax Planning Guide

Key Strategies for Business Owners Before 30 June 2026

Why Act Before 30 June?

Key Tax Planning Strategies

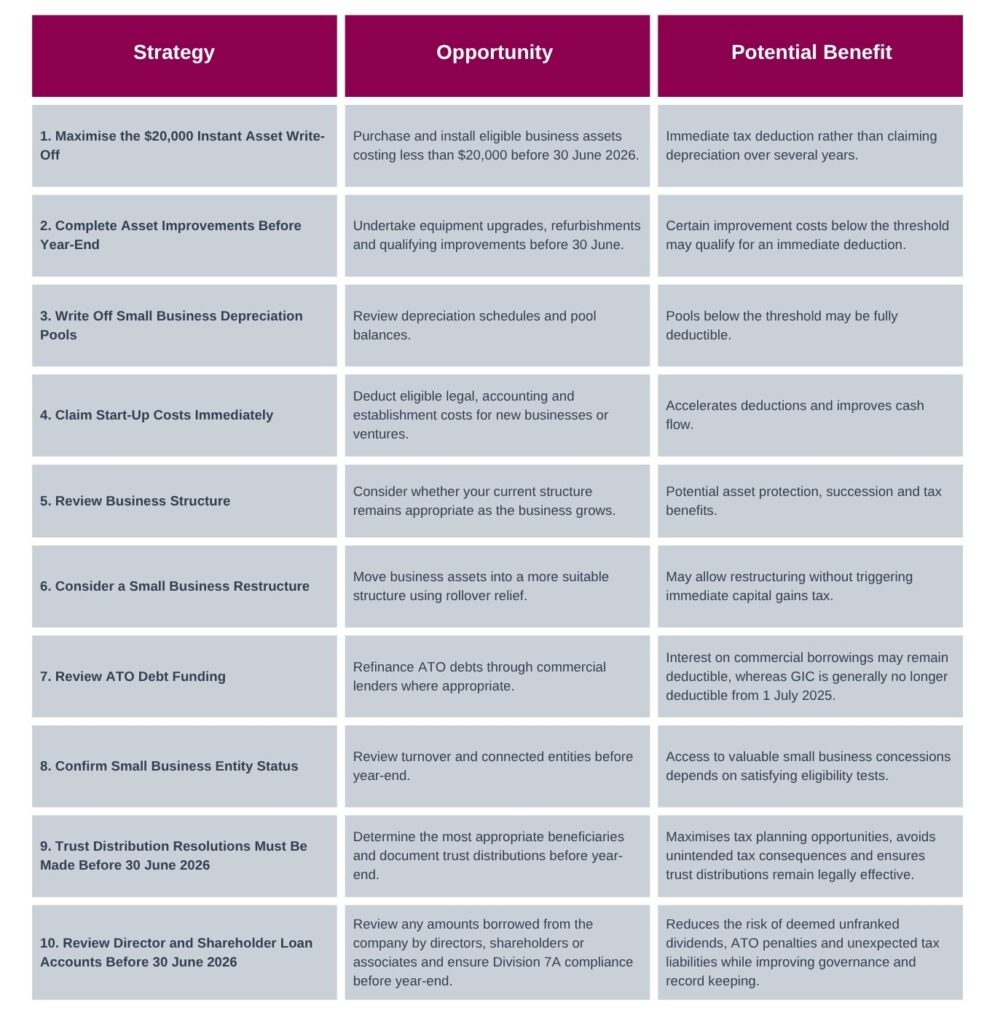

Strategy 1: Take Advantage of the $20,000 Instant Asset Write-Off

For eligible Small Business Entities, assets costing less than $20,000 may be immediately deductible if they are:

- Purchased before 30 June 2026;

- Installed and ready for use by 30 June 2026; and

- Used in the business.

Examples include:

- Vehicles

- Machinery

- Office equipment

- Computers

- Business technology

- Tools and equipment

Important

The business must not simply order the asset. It must be installed and ready for use before 30 June 2026.

Strategy 2: Bring Forward Improvement Expenditure

Many businesses focus on buying new assets but overlook upgrades to existing assets.

Examples include:

- Machinery upgrades

- Technology enhancements

- Equipment modifications

- Productivity improvements

Where conditions are met, these costs may qualify for immediate deduction treatment.

Strategy 3: Review ATO Debt Arrangements

A major change applies from 1 July 2025.

General Interest Charge (GIC) and Shortfall Interest Charge (SIC) are no longer generally deductible. Businesses carrying significant ATO debt should review whether refinancing through a commercial lender may improve their after-tax position.

Strategy 4: Consider a Business Restructure

As businesses grow, their original structure may no longer be optimal.

Common reasons to restructure include:

- Asset protection

- Succession planning

- Bringing family members into ownership

- Separating trading and investment assets

- Preparing for a future sale

The Small Business Restructure Rollover may allow certain restructures to occur without triggering immediate tax consequences.

Strategy 5: Review Business Eligibility for Small Business Concessions

Many valuable tax concessions depend on meeting turnover thresholds and Small Business Entity rules.

Before 30 June, businesses should review:

- Annual turnover

- Connected entities

- Affiliate relationships

- Group structures

This review may preserve access to depreciation concessions and other tax benefits.

Strategy 6: Consider a Small Business Restructure

As businesses grow, their original structure may no longer be optimal.

Common reasons to restructure include:

- Asset protection

- Succession planning

- Bringing family members into ownership

- Separating trading and investment assets

- Preparing for a future sale

The Small Business Restructure Rollover may allow certain restructures to occur without triggering immediate tax consequences.

Strategy 7: Review ATO Debt Funding

A major change applies from 1 July 2025.

General Interest Charge (GIC) and Shortfall Interest Charge (SIC) are no longer generally deductible. Businesses carrying significant ATO debt should review whether refinancing through a commercial lender may improve their after-tax position.

Strategy 8: Confirm Small Business Entity Status

Many valuable tax concessions depend on meeting turnover thresholds and Small Business Entity rules.

Before 30 June, businesses should review:

- Annual turnover

- Connected entities

- Affiliate relationships

- Group structures

This review may preserve access to depreciation concessions and other tax benefits.

Strategy 9: Trust Distribution Resolutions Must Be Made Before 30 June 2026

A discretionary trust generally does not automatically distribute its income. The trustee must determine who is entitled to the trust income for the year.

If no valid resolution is made by the required date:

- The trustee may lose flexibility over who receives trust income.

- The trust deed’s default beneficiary provisions may apply.

- The trustee may be assessed on trust income at the highest marginal tax rate.

- The intended tax planning outcome may not be achieved.

- There may be increased risk of ATO review, particularly where family groups utilise bucket companies or streaming arrangements.

Strategy 10: Review Director and Shareholder Loan Accounts Before 30 June 2026

If your business operates through a company, it is important to review all director, shareholder and associate loan accounts before 30 June 2026.

The ATO continues to scrutinise Division 7A arrangements, particularly where private company funds have been used for personal purposes or where loan balances remain unpaid.

Year-End Business Checklist

Before 30 June 2026

☐ Review eligibility as a Small Business Entity

☐ Purchase and install eligible assets under $20,000

☐ Complete planned equipment upgrades and improvements

☐ Review depreciation pool balances

☐ Claim eligible start-up and establishment costs

☐ Review outstanding ATO tax debts

☐ Consider refinancing ATO liabilities

☐ Review business structure for asset protection and succession planning

☐ Assess whether a Small Business Restructure Rollover may be appropriate

☐ Prepare Trust resolutions prior to 30 June 2026

☐ Review director, shareholder and associate loan accounts for Division 7A compliance before 30 June 2026.

☐ Arrange a tax planning meeting with Paula before 30 June.

Disclaimer

This publication is intended as a general guide only and is not intended to constitute taxation, accounting, financial, investment or legal advice. The information provided does not take into account your personal objectives, financial situation, business structure or individual circumstances.

The suitability and effectiveness of any strategy referred to in this publication will depend on your particular circumstances and the application of taxation laws at the relevant time. Before implementing any strategy, you should obtain professional advice tailored to your specific circumstances.

While every effort has been made to ensure the accuracy of the information contained in this publication, Hart Partners accepts no responsibility for any loss or liability arising from reliance on this information.

Liability limited by a scheme approved under Professional Standards Legislation.